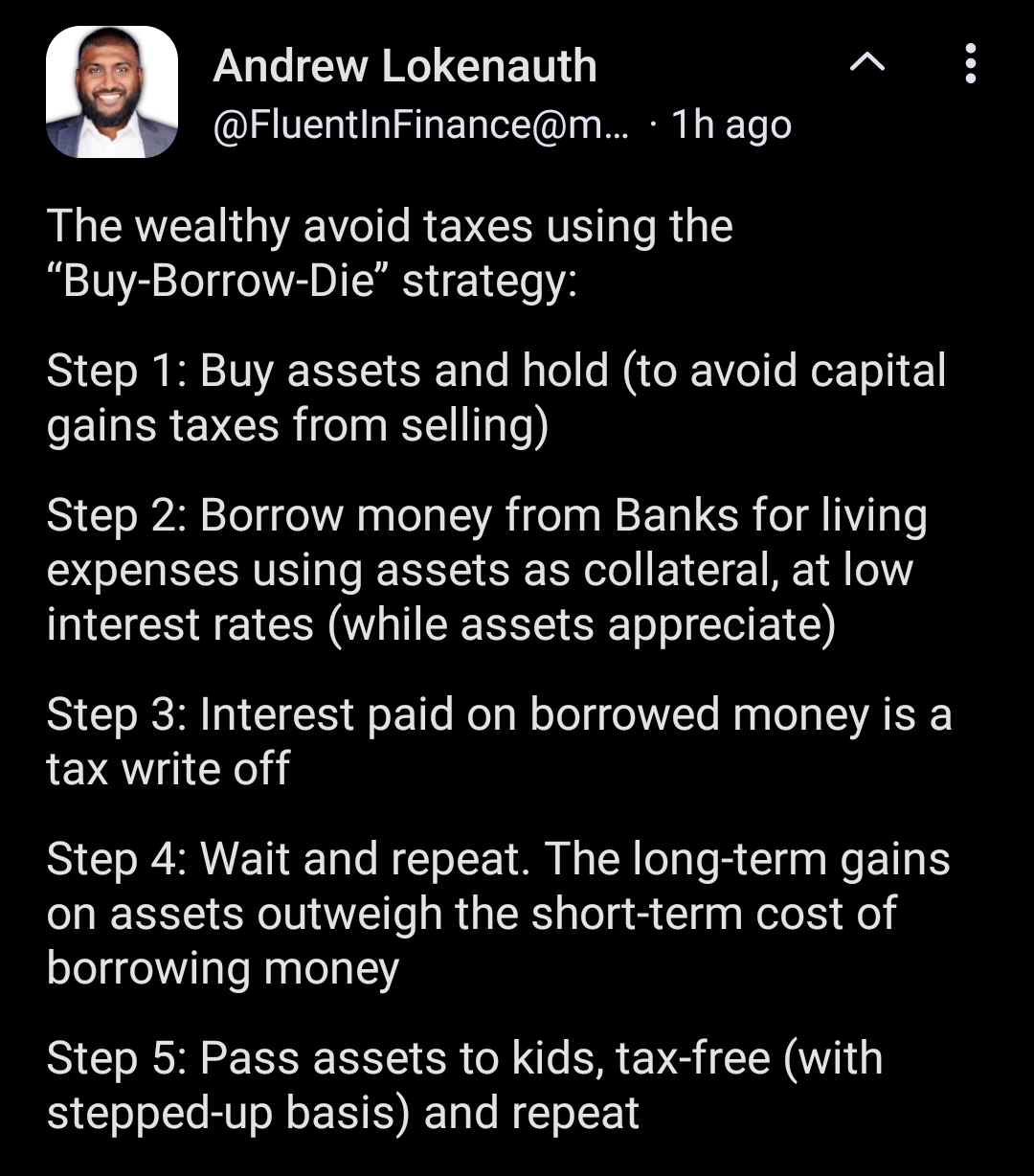

Hypothetical: Assets like land and housing are reliably expected to only increase in value.

Once one loan runs out, the assets are worth more and a new loan will be potentially considerably more than the previous.

As a second hypothesis, I suspect that fractional reserve banking plays heavily into this.

I don’t think fractional reserve banking is necessary here. Fractional reserve banking just makes it easier for banks to make loans, it has little to do with rich people taking advantage of tax law.

For example, the most obvious loan is a margin loan, which doesn’t require any fractional reserve banking whatsoever. Quite often brokerages will offer margin loans backed by the assets themselves and force you to sell if you go under a certain loan to value limit, which means the risk is incredibly low. Banks will then use the loans as a replacement for savings accounts to earn reliable interest on cash assets, so it doesn’t need to be tied to reserve rates. However, if reserve rates are lower, they’d probably take advantage.

In fractional reserve banking, banks make loans with deposits, and they make more loans using those loans as assets, and federal rules stipulate that they need you have a certain percentage of the loan values liquid (i.e. so depositors don’t lose their money). With margin loans, they don’t use savings deposits to make loans (there are no savings deposits, everything is invested in a fund), they instead use brokerage assets. So there’s no fractional reserve system at all because the only ones impacted are the brokerage themselves.

{kind=link}

Hypothetical: Assets like land and housing are reliably expected to only increase in value.

Once one loan runs out, the assets are worth more and a new loan will be potentially considerably more than the previous.

As a second hypothesis, I suspect that fractional reserve banking plays heavily into this.

I don’t think fractional reserve banking is necessary here. Fractional reserve banking just makes it easier for banks to make loans, it has little to do with rich people taking advantage of tax law.

For example, the most obvious loan is a margin loan, which doesn’t require any fractional reserve banking whatsoever. Quite often brokerages will offer margin loans backed by the assets themselves and force you to sell if you go under a certain loan to value limit, which means the risk is incredibly low. Banks will then use the loans as a replacement for savings accounts to earn reliable interest on cash assets, so it doesn’t need to be tied to reserve rates. However, if reserve rates are lower, they’d probably take advantage.

In fractional reserve banking, banks make loans with deposits, and they make more loans using those loans as assets, and federal rules stipulate that they need you have a certain percentage of the loan values liquid (i.e. so depositors don’t lose their money). With margin loans, they don’t use savings deposits to make loans (there are no savings deposits, everything is invested in a fund), they instead use brokerage assets. So there’s no fractional reserve system at all because the only ones impacted are the brokerage themselves.